Private Loan Considerations

When considering loans to finance your Columbia University education, you can start here to make informed borrowing decisions. Below, we have provided actionable tools to help you begin securing a private loan.

Congress passed the One Big Beautiful Bill Act (OBBBA) in July 2025, which introduced several changes to federal student loans beginning July 1, 2026. Please find those Updates to the Federal Student Loan Limits for AY26-27 here.

For more information about federal loans please visit our Federal Loans Pages:

How Much do I Need?

Private student loans can help bridge the gap after you've exhausted scholarships, personal funds, and federal aid, though you should always prioritize federal loans first for their advantageous repayment benefits and protections. If you must borrow privately, applying with a creditworthy cosigner is highly recommended to improve your approval odds and secure more favorable interest rates.

You can find more information about private loans here.

Before applying for a private loan, it is important to determine exactly how much you will need for your period of enrollment. If a formal bill has not yet been generated - the billing schedule is here, you can estimate your costs by reviewing the Tuition and Fees page. To view your actual billed charges, review your financial aid package, and calculate your remaining gap, please navigate to Manage Student Accounts..

We also encourage you to contact your financial aid office and make an appointment with your counselor to review this information and solidify your financing strategy.

If you have specific private loan questions, please submit them here.

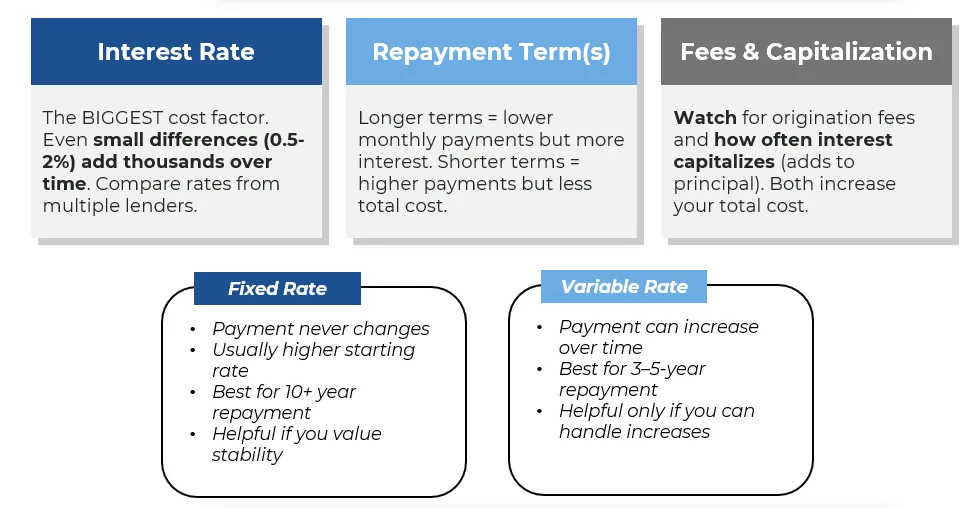

How to Pick a Private Loan

- Check your credit report: Visit annualcreditreport.com for a free report. Review it closely for errors and to understand your current standing.

- Manage your utilization and history: Lower your credit utilization (ideally below 30%), keep your oldest accounts open to maintain a long credit history, and ensure every payment is made on time.

- Limit new inquiries: Keep new credit applications to a minimum. Applying for multiple lines of credit—including "buy now, pay later" tools—triggers "hard inquiries," which can ding your score.

- Rate-shop strategically: When applying for student loans, submit all applications within a short window (usually two weeks). Credit bureaus will treat these as a single "hard inquiry" since they share the same purpose. Some lenders offer soft credit check tools that let you preview rates without affecting your credit but keep in mind these estimates are not always accurate. Similarly, if you use loan comparison sites, be aware that many are not fully independent. Some sites receive compensation for promoting certain lenders, which can influence their rankings or recommendations.

- Consider a co-signer: Determine if you have access to a creditworthy co-signer. Their support can significantly expand your options and help you land a lower interest rate.

Borrow Only What You Need

Calculate your actual expenses: tuition and fees not covered by other aid, books and supplies, living expenses, and transportation. Then borrow that amount, not the maximum available. Every extra dollar you borrow costs you approximately $1.50-2.00 to repay depending on interest rate and term.

Make Interest Payments While in School

Even small payments toward interest can save you thousands by preventing capitalization. Example: On a $30,000 loan at 6% on a 10-year repayment plan while in school for 4 years, if you pay $0, interest capitalizes to $37,200 principal at graduation. If you pay $150/month during school (i.e., just enough to cover accruing interest), you keep principal at $30,000 and save over $2400 over the life of the loan.

When you make zero payments while in school, the $7,200 of interest that accrues over those four years is added to your original loan amount when you graduate. This process is called capitalization, and it turns your $30,000 loan into a $37,200 loan.

During your 10-year repayment period, the lender charges you 6% interest on that new, higher balance. Because you are now being charged interest on the $7,200 that was added to your account, you are essentially paying interest on your interest. By making the $150 payments while in school, you prevent that $7,200 from ever being added to your principal balance. You only ever pay interest on your original $30,000. By keeping your principal balance lower and stopping compound interest from snowballing, you prevent the loan from becoming artificially expensive and save yourself roughly $2,400 in the long run.

Consider Making Payments During the Grace Period

Don't wait until you must start paying. Any payments during the grace period reduce your principal before interest capitalizes.

Set Up Autopay

Most lenders offer a 0.25% rate reduction for automatic payments. Many lenders include this option while you’re in school, including payments that just cover interest or (sometimes) are as low as $1/month. That's free money, take it!

When applying for a private loan, request only the exact amount needed to cover your calculated gap, choosing the lender that offers the best terms for your situation. If you plan to apply with multiple lenders to compare rates, we recommend submitting all applications within a two-week window. This allows you to shop for the most competitive offers while minimizing the impact of hard inquiries on your credit score.

Final Checklist before you Sign

Before you commit to any loan, make sure you:

- Compare at least 2 lenders using the comparison checklist

- Understand whether you prefer a fixed or variable rate

- Know your exact monthly payment amount

- Calculate the total amount you'll repay over the loan's lifetime

- Read and understood all fees

- Know how often interest capitalizes

- Find and discuss all relevant terms and conditions with a co-signer (if applicable)

- Choose the shortest repayment term you can afford

- Confirm you’re only borrowing what you need

- Put together a plan for making payments after graduation

Private educational loans are disbursed in a variety of ways. Some lenders send funds directly to Columbia University, others send funds to the student borrower directly .

Ensure Columbia certifies your private loan and confirm all loan funds are scheduled to disburse before payment deadlines. You can confirm this by looking at your Student Account activity in SSOL.